Table of Content

- What is Financial Software Development?

- Why Financial Software Development Matters in 2026

- Types of Financial Software: What Are You Actually Building?

- Digital Banking Platforms

- Payment Processing Systems

- Accounting and Financial Management Software

- Lending and Credit Platforms

- Investment and Wealth Management Platforms

- Fraud Detection and Risk Management Software

- Insurance Technology (InsurTech) Platforms

- RegTech (Regulatory Technology) Solutions

- Custom Financial Software vs. Off-the-Shelf Solutions

- When Off-the-Shelf Makes Sense

- When Custom Development is the Right Choice

- Core Features Every Financial Software Must Have in 2026

- Multi-Layer Security Architecture

- Compliance and Regulatory Controls Built Into the Architecture

- Real-Time Payment Processing and Multi-Rail Support

- AI-Powered Fraud Detection

- Scalable Cloud-Native Architecture

- Comprehensive Reporting and Analytics

- API Integration Layer

- The Technology Stack for Financial Software Development in 2026

- Frontend Technologies

- Backend Technologies

- Databases

- Specialized Financial Tools

- The Financial Software Development Process: Step by Step

- Step 1 - Discovery and Requirements Analysis

- Step 2 - UI/UX Design

- Step 3 - Architecture Planning and Technology Selection

- Step 4 - Development in Iterative Sprints

- Step 5 - Security Testing and Compliance Audits

- Step 6 - Deployment and Launch

- Step 7 - Ongoing Maintenance and Evolution

- What Does Financial Software Development Actually Cost? Understanding the Real Factors

- Factor 1 - Project Scope and Feature Complexity

- Factor 2 - Compliance and Security Requirements

- Factor 3 - Integration with Existing Systems

- Factor 4 - Team Composition and Engagement Model

- Factor 5 - Architecture and Infrastructure Decisions

- Factor 6 - Ongoing Maintenance and Support

- Cost Estimation Approaches

- Top Trends Shaping Financial Software Development in 2026

- AI and Machine Learning Are Now Baseline, Not Premium

- Embedded Finance Is Reshaping the Market

- Cloud-Native Architecture Is Replacing Legacy Systems

- RegTech Is Now a Core Component, Not an Add-On

- Open Banking and API-First Development

- Enhanced Biometric Security

- Common Mistakes That Sink Financial Software Projects

- Answers to Common Questions About Financial Software Development

- What is the difference between fintech software and financial software?

- How long does it take to build financial software?

- What compliance does financial software need in 2026?

- Should I build custom financial software or use an existing platform?

- What technologies are used in financial software development?

- How do I choose a financial software development company?

- Digisoft Solution: Top Financial Software Development Partner

- We Start With Compliance, Not Code

- Security Architecture That Is Built In, Not Bolted On

- Full-Stack Financial Software Development

- Integration Expertise Where It Matters Most

- Our Financial Software Development Services Include

- Frequently Asked Questions

- Is financial software development regulated?

- How do I protect my financial software from data breaches?

- What is open banking and how does it affect software development?

- How do I estimate the ROI of a custom financial software project?

- Do I need a dedicated maintenance team after launch?

- Final Thoughts: Building Financial Software That Actually Works

Digital Transform with Us

Please feel free to share your thoughts and we can discuss it over a cup of coffee.

If you are a business owner, a startup founder, or someone working in the financial services industry, you have probably already felt it. The way companies handle money, transactions, compliance, and customer data has changed dramatically in the last few years. And in 2026, that change is only accelerating.

Financial software development is no longer something only large banks or Wall Street firms think about. Businesses of all sizes, from fintech startups to mid-size accounting firms to enterprise-level financial institutions, are investing in custom software to stay competitive, stay compliant, and frankly, just to keep up.

This guide breaks everything down for you: what financial software actually is, what types exist, what features matter, how compliance works, what the real cost factors are, and how to pick the right development partner. We have also included a dedicated section on how Digisoft Solution helps businesses build secure, scalable financial platforms.

What is Financial Software Development?

Financial software development is the process of designing, building, testing, and maintaining digital applications that handle financial data, transactions, reporting, and regulatory compliance. These are not generic business apps. They are purpose-built systems that need to handle real money, sensitive personal data, and strict legal requirements.

Whether it is a mobile banking app, an investment portfolio management tool, a payroll system, or a real-time fraud detection engine, financial software is at the core of how modern businesses operate.

What separates it from regular software development is the regulatory burden. Every single feature that touches financial data, whether it stores account numbers, processes payments, or generates tax reports, must satisfy specific legal and security standards. That is not optional complexity. That is the baseline requirement.

Why Financial Software Development Matters in 2026

The numbers make the case pretty clearly. The global financial management software market is projected to reach $16.2 billion in 2026, growing at a 9.7% compound annual growth rate. The enterprise segment alone is expected to hit $14.11 billion at a 17.2% CAGR.

But beyond the market stats, here is what is really driving this growth:

- Customers expect real-time, mobile-first financial experiences

- Regulators are tightening compliance requirements across every region

- Legacy systems simply cannot keep up with modern transaction volumes

- AI and automation are creating new possibilities in fraud detection, credit scoring, and financial forecasting

- The rise of embedded finance means even non-financial companies are building financial features into their products

A recent McKinsey report found that over 92% of companies plan to increase their technology investment in the next three years. The pressure from customers, competitors, and regulators is all pointing in the same direction: businesses that invest in financial software now will be the ones leading their markets in the next five years.

Types of Financial Software: What Are You Actually Building?

Before you can plan a development project, you need to know what category of financial software you are actually building. Each type comes with its own technical requirements, compliance considerations, and cost drivers.

Digital Banking Platforms

These are web and mobile applications that let users manage accounts, make transfers, view transaction history, and access personalized financial insights. Whether you are building a full neobank or a mobile banking layer on top of an existing core banking system, digital banking platforms are among the most complex categories to build correctly.

Key features: account management, real-time transaction feeds, push notifications, biometric login, multi-currency support, and open banking API integrations.

Payment Processing Systems

Payment software handles the movement of money between parties, whether that is card processing, bank transfers, digital wallets, or cross-border remittance. In 2026, modern payment platforms need to support multiple rails including ACH, SEPA, UPI, and digital wallet networks like Apple Pay and Google Pay.

Key features: multi-gateway integration, real-time settlement, fraud prevention, PCI-DSS compliance, and multi-currency processing.

Accounting and Financial Management Software

These systems automate financial record-keeping, invoicing, payroll, expense tracking, and tax calculations. Enterprise-level platforms go much further, handling multi-entity reporting, intercompany consolidations, and regulatory documentation across multiple jurisdictions.

For reference, JPMorgan's COiN platform processes more than 12,000 loan agreements in seconds, work that previously took 360,000 human hours per year. That is what custom financial software automation can look like at scale.

Lending and Credit Platforms

Automated lending systems streamline risk assessment, underwriting, and collections. They integrate with credit bureaus, AML/KYC providers, and banking APIs to make faster, smarter lending decisions while reducing default risk.

Key features: credit scoring engine, KYC/AML workflows, loan origination, repayment tracking, and regulatory reporting.

Investment and Wealth Management Platforms

These include portfolio management tools, robo-advisors, trading platforms, and reporting dashboards for asset managers. They need to handle complex financial instruments, real-time market data feeds, and sophisticated compliance requirements.

Fraud Detection and Risk Management Software

AI-powered fraud detection systems monitor transactions in real time, flagging suspicious patterns before they become losses. These systems use machine learning models trained on historical transaction data to distinguish between legitimate activity and fraud with high accuracy.

Insurance Technology (InsurTech) Platforms

InsurTech software automates policy management, claims processing, premium calculations, and regulatory reporting for insurance providers. These platforms often integrate with IoT devices, medical records systems, and third-party data providers.

RegTech (Regulatory Technology) Solutions

RegTech is now a standalone industry. Financial software in 2026 increasingly includes built-in compliance tools: AML detection, KYC automation, real-time regulatory reporting, and audit trail management. These capabilities are not optional add-ons anymore. They are expected from day one.

Custom Financial Software vs. Off-the-Shelf Solutions

This is one of the most common questions businesses ask when starting a financial software project. And honestly, it is not a simple answer because it depends on where your business actually is right now.

When Off-the-Shelf Makes Sense

There are situations where buying an existing solution is the smarter move. If your financial processes are fairly standard, like basic invoicing, payroll, or simple accounting, a well-supported platform like QuickBooks or Xero might cover 95% of what you need. Off-the-shelf tools get you live fast, the vendor handles updates and security patches, and the per-seat cost is usually attractive early on.

Choose off-the-shelf when:

- Your processes are standard and do not involve proprietary business logic

- Your compliance requirements are covered by the platform's existing certifications

- You are still validating your business model and need to move fast

- You do not have dedicated technical resources for custom maintenance

When Custom Development is the Right Choice

Custom financial software development makes the most sense when your workflows involve proprietary business logic that cannot be replicated with configuration, when you need integrations that off-the-shelf tools simply do not support, or when your compliance requirements demand full control over how data is stored and processed.

The hidden cost of off-the-shelf solutions is vendor lock-in. When your financial data lives inside a third-party platform, switching costs escalate over time. Custom software built on open standards and your own infrastructure eliminates that dependency.

Choose custom development when:

- Your business logic is proprietary and not replicable through configuration

- You need full control over data storage and processing for compliance reasons

- Existing tools require so many workarounds that maintenance costs approach custom development costs anyway

- You need integrations with legacy systems or specialized financial APIs that no off-the-shelf tool supports

- You are building a product that needs to be clearly differentiated from competitors

Core Features Every Financial Software Must Have in 2026

Regardless of what type of financial software you are building, there is a set of capabilities that are non-negotiable in 2026. These are not nice-to-haves. They are baseline requirements.

Multi-Layer Security Architecture

In 2026, security is not a feature you bolt on after the product is built. It is the foundation everything else is built on. Financial institutions face the second-highest data breach costs of any industry, averaging $6.08 million per incident according to IBM's 2024 Cost of a Data Breach Report.

What this means practically:

- End-to-end encryption for data in transit and at rest

- Field-level encryption so even database administrators cannot read sensitive payment details in plain text

- Tokenization of card numbers and account details

- Multi-factor authentication (MFA) including biometric options

- Role-based access controls (RBAC) with principle of least privilege

- Real-time anomaly detection and behavioral monitoring

- Regular penetration testing and vulnerability assessments

Compliance and Regulatory Controls Built Into the Architecture

Compliance is not a feature you add at the end of a financial software project. It is an architectural decision that affects database design, API structure, authentication flows, and data storage from the very first sprint.

Key compliance frameworks your software may need to address:

- PCI-DSS: Required for any system that processes, stores, or transmits cardholder data

- GDPR: Mandatory for businesses handling personal data of EU residents

- SOC 2: Required for SaaS financial products handling customer data

- AML (Anti-Money Laundering): Automated monitoring of suspicious transactions

- KYC (Know Your Customer): Identity verification workflows for user onboarding

- ISO/IEC 27001: Information security management for enterprise systems

- CCPA: For businesses handling California residents' personal data

Real-Time Payment Processing and Multi-Rail Support

Financial software in 2026 must support multiple payment rails. Your platform should handle card networks, bank transfers (ACH, SEPA, Faster Payments), digital wallets, and local payment methods relevant to your target markets. Real-time payment tracking and instant notifications have become expected, not exceptional.

AI-Powered Fraud Detection

AI has moved beyond a luxury for financial applications. Modern fraud detection systems use machine learning to flag suspicious transactions before they are processed. They also adapt over time as fraud patterns evolve, which static rule-based systems simply cannot do.

Applications of AI in financial software:

- Real-time transaction anomaly detection

- Credit scoring through machine learning models

- Predictive fraud alerts before payment processing completes

- Personalized financial recommendations based on spending patterns

- Automated compliance risk identification

- Natural language processing for document review and contract analysis

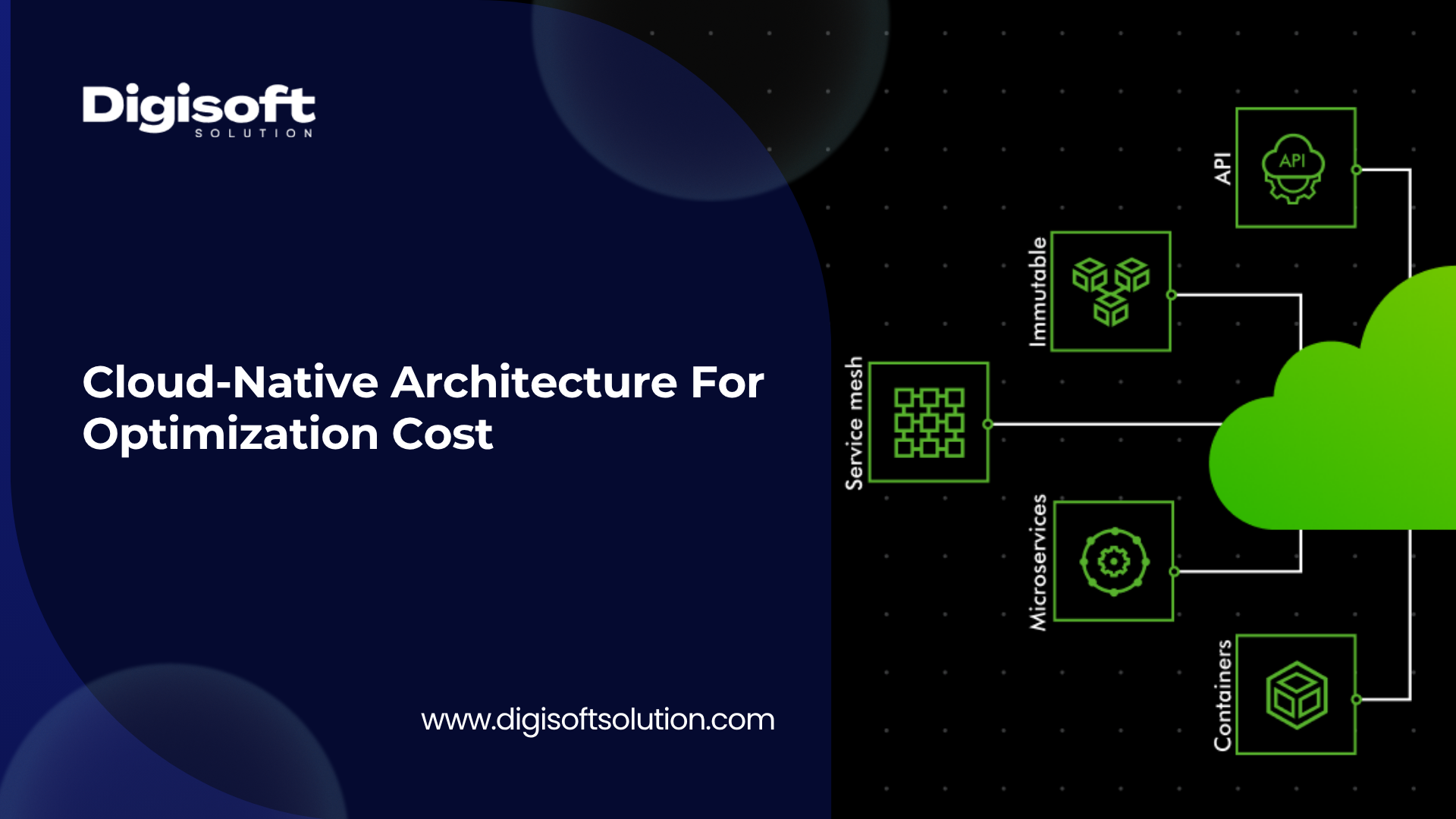

Scalable Cloud-Native Architecture

Financial institutions are moving away from legacy monolithic systems to modular, cloud-native platforms using microservices and containerization. This approach gives you greater agility, scalability, and resilience, meaning your system can handle significantly higher transaction volumes without a complete rebuild.

- Microservices vs. monolithic architecture decisions

- Cloud-native vs. on-premises vs. hybrid deployment

- API-first design for open banking integrations

- Event-driven architecture for real-time processing

- Database design that supports audit trails from day one

Comprehensive Reporting and Analytics

Financial stakeholders, from CFOs to regulators to customers, all want visibility into financial data. Modern financial software needs built-in reporting dashboards, automated regulatory reports, and data export capabilities that work across multiple formats and jurisdictions.

API Integration Layer

Modern financial platforms do not operate in isolation. They connect to payment gateways, banking APIs, credit bureaus, KYC providers, insurance systems, and tax authorities. A well-designed API integration layer is what makes your financial software extensible and future-proof.

The Technology Stack for Financial Software Development in 2026

Choosing the right technology stack is one of the most consequential decisions in a financial software project. The wrong choice creates technical debt that becomes very expensive to fix later.

Frontend Technologies

For web interfaces, React and Angular remain dominant choices in 2026 due to their robust ecosystem, strong community support, and performance characteristics. For mobile, React Native and Flutter are widely used for cross-platform financial apps. Native iOS (Swift) and Android (Kotlin) development is still preferred for performance-critical banking applications.

Backend Technologies

Python is widely used for AI/ML components, data processing pipelines, and financial analytics. Java and Kotlin are preferred for high-throughput transaction processing due to strong concurrency handling. Node.js works well for real-time communication layers and API gateways. Go is gaining adoption for performance-critical financial systems requiring low latency.

Databases

PostgreSQL is the default choice for transactional financial data due to its ACID compliance, reliability, and strong support for complex queries. MongoDB is used for flexible document storage. Redis handles caching and session management. TimescaleDB works well for time-series financial data.

Specialized Financial Tools

- TensorFlow and PyTorch for AI/ML fraud detection models

- Apache Kafka for real-time event streaming and transaction processing

- Hyperledger Fabric for permissioned blockchain applications

- HashiCorp Vault for secrets management and encryption key handling

- Kong or AWS API Gateway for API management and rate limiting

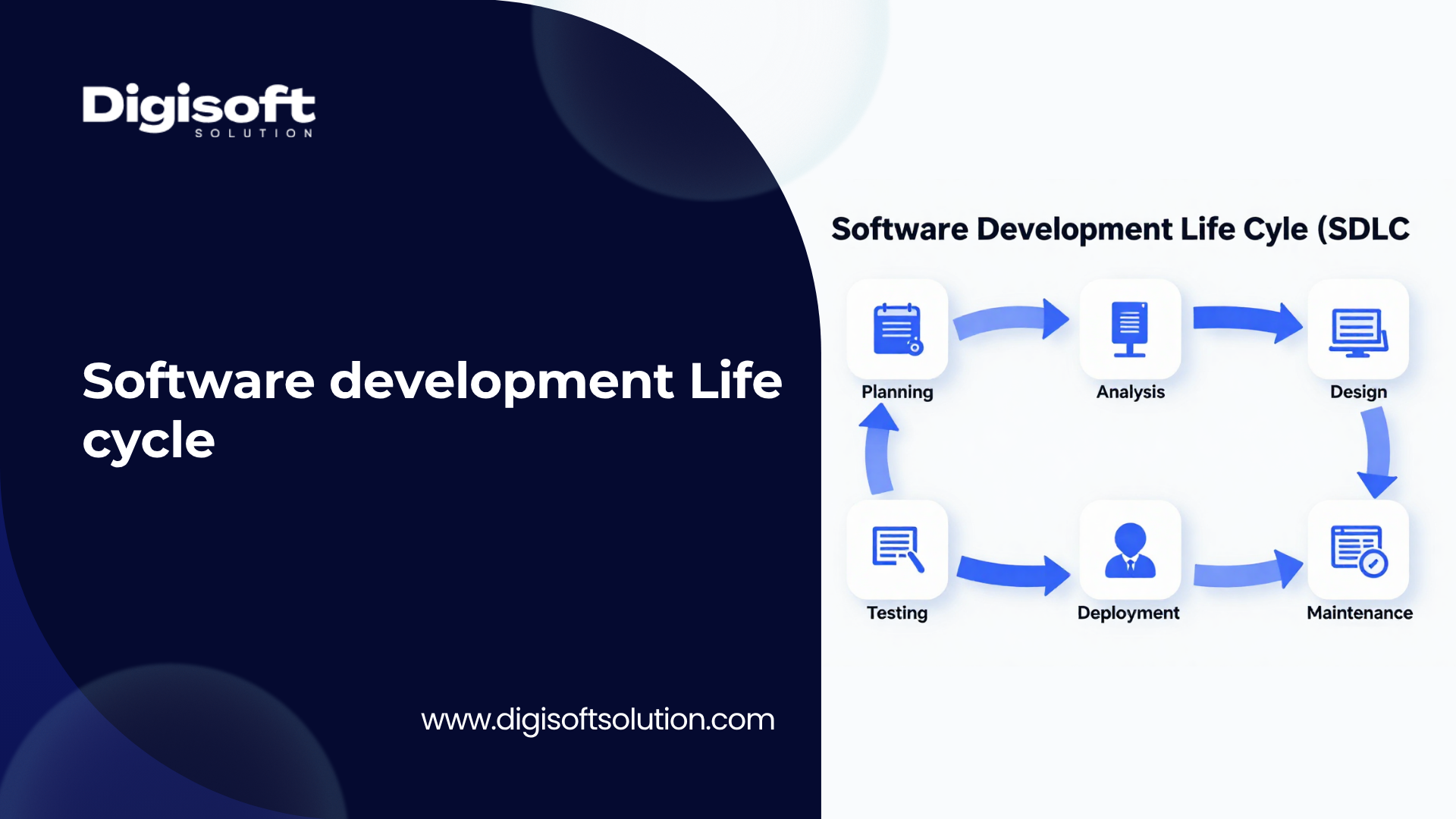

The Financial Software Development Process: Step by Step

Building financial software is not just about writing code. It is a structured process that, when done right, produces systems that are secure, compliant, and built to last.

Step 1 - Discovery and Requirements Analysis

This is where you define what you are building, why, and for whom. A thorough discovery phase maps your compliance requirements, identifies integration points with existing systems, and defines the architecture before any code is written. Skipping or rushing this phase is one of the most common reasons financial software projects exceed their budget.

Discovery outputs:

- Technical requirements document

- Compliance framework definition

- System architecture diagram

- API integration map

- Risk assessment report

- Project timeline and budget estimate

Step 2 - UI/UX Design

Financial interfaces must be intuitive, transparent, and resistant to user error. Poor UX in financial software does not just frustrate users. It increases error rates, reduces trust, and in some cases creates compliance issues. A good design process involves user research, wireframing, interactive prototyping, and accessibility testing.

Step 3 - Architecture Planning and Technology Selection

Before writing a single line of code, the system architecture must be defined. This includes database schema design (which must account for audit trail requirements from day one), API structure, authentication flows, data storage strategy, and infrastructure planning.

Step 4 - Development in Iterative Sprints

Modern financial software is built using agile methodology, typically in two-week sprints. This approach gives you visibility into progress, allows for course corrections, and ensures compliance requirements are validated continuously rather than at the very end.

- Core infrastructure and security framework

- Authentication and authorization system

- Core business logic and financial processing

- API integrations (payment gateways, banking APIs, KYC providers)

- Reporting and analytics modules

- Admin dashboard and monitoring tools

Step 5 - Security Testing and Compliance Audits

Before launch, a comprehensive security audit is mandatory. This includes penetration testing by independent security teams, vulnerability assessment across all system components, PCI-DSS compliance audit if applicable, and load testing to verify system stability under peak transaction volumes.

Step 6 - Deployment and Launch

Financial software deployments require careful planning. A phased rollout approach reduces risk, starting with a limited user base and scaling up as stability is confirmed. Infrastructure monitoring, automated alerting, and incident response procedures should all be in place before go-live.

Step 7 - Ongoing Maintenance and Evolution

Financial regulations change. Threat landscapes evolve. Business requirements expand. Ongoing maintenance is not optional, it is built into the cost structure of any serious financial software project. Plan for 15-25% of your initial build cost annually for maintenance, security updates, and feature development.

What Does Financial Software Development Actually Cost? Understanding the Real Factors

We want to be straight with you about this section. We are not going to give you a single number and call it a day, because anyone who does that is either guessing or oversimplifying. The real cost of financial software development is driven by a set of factors that vary enormously depending on what you are building.

What we will do is break down each cost driver so you can understand what actually makes financial software more or less expensive, and make informed decisions about where to invest.

Factor 1 - Project Scope and Feature Complexity

The single biggest cost driver is what you are building. A simple expense tracking tool and a full-scale digital banking platform with lending, payments, and investment features are fundamentally different projects. Each additional module, workflow, and integration adds development hours and testing requirements. Starting with a well-defined MVP is a smart strategy for most projects.

Factor 2 - Compliance and Security Requirements

This is the cost driver most teams underestimate. Regulatory compliance is not a feature you add at the end. It is built into the architecture from day one, and it adds significant technical work. PCI-DSS certification requires specific technical controls. SOC 2 compliance involves independent auditing. GDPR compliance requires data architecture decisions that affect your entire database design.

Budget at least 15-25% extra time beyond feature development for compliance-related work. Teams that ignore this consistently exceed their original budget.

Factor 3 - Integration with Existing Systems

This is often the most underestimated cost driver of all. If your new financial software needs to pull historical data from existing systems, reconcile formats across multiple sources, or maintain real-time synchronization with external platforms, plan for that work to consume 20-30% of your total development budget.

- Payment gateway integrations: each adds roughly 2-4 weeks of development and testing

- Core banking system integrations: often legacy systems with poor documentation, highly unpredictable timelines

- KYC/AML provider integrations: require careful testing due to compliance implications

- Credit bureau integrations: vary significantly by region and provider

- Custom ERP or CRM integrations: depends entirely on the specific system

Factor 4 - Team Composition and Engagement Model

Financial software development requires specialized skills beyond standard web development: security architecture expertise, financial domain knowledge, compliance experience, and AI/ML capabilities for advanced features. Geographic location also affects cost. The important thing to focus on is not just hourly rate but total cost of delivery, which includes project management overhead, communication efficiency, timezone alignment, and domain expertise in financial systems.

Factor 5 - Architecture and Infrastructure Decisions

Microservices architecture costs more to build initially than a monolith but scales better and is easier to maintain long-term. Cloud infrastructure choices affect both initial setup costs and ongoing operational expenses. The decision between cloud, on-premises, or hybrid deployment has compliance implications, especially for organizations subject to data residency requirements.

Factor 6 - Ongoing Maintenance and Support

Financial software is never truly done. Plan to budget 15-25% of your initial build cost annually for maintenance, security patches, compliance updates, and feature development. This is not optional spending. It is the cost of operating compliant, secure financial software in a constantly changing regulatory environment.

Cost Estimation Approaches

|

Estimation Model |

Best Used When |

Key Considerations |

|

Fixed-Price Model |

Requirements are very clearly defined upfront |

Scope changes become expensive; vendor carries risk |

|

Time and Material |

Requirements may evolve; complex integrations expected |

Better flexibility; requires active client oversight throughout |

|

Sprint-Based Model |

Agile development with ongoing feature additions |

Most transparent; gives full control over scope and budget at each stage |

|

MVP First Approach |

Validating product before full capital investment |

Reduces initial risk; plan carefully for subsequent build phases |

The bottom line on cost: financial software is a significant investment, and the projects that succeed are the ones where teams invest in proper discovery upfront, account for compliance work realistically, and plan for ongoing maintenance from day one. Projects that fail, or far exceed budget, are usually the ones that underestimate compliance requirements, rush discovery, or treat security as an afterthought.

Top Trends Shaping Financial Software Development in 2026

AI and Machine Learning Are Now Baseline, Not Premium

In 2026, AI is not a luxury feature in financial software. It is an expected capability. Financial applications now use AI for fraud detection before payment processing, real-time credit scoring, personalized financial advice based on individual spending patterns, and compliance risk identification before issues occur. Agentic AI systems that can execute financial tasks without manual intervention are the next frontier, and early adopters are already building competitive advantages through these capabilities.

Embedded Finance Is Reshaping the Market

Financial services are being integrated directly into non-financial platforms, from e-commerce sites to logistics software to HR platforms. This trend creates new opportunities for businesses to build financial capabilities into their core products, and for financial software development companies to support that integration work.

Cloud-Native Architecture Is Replacing Legacy Systems

Financial institutions are migrating from legacy monolithic systems to modular, cloud-native platforms. This migration is one of the largest sources of financial software development work in 2026, and it is creating opportunities for companies that have experience bridging legacy and modern systems.

RegTech Is Now a Core Component, Not an Add-On

In 2026, financial applications increasingly have built-in AML detection using machine learning, automated KYC workflows, real-time regulatory reporting, and audit trail automation. These are expected capabilities, not premium features.

Open Banking and API-First Development

Open banking regulations are expanding globally, requiring financial institutions to expose their services through standardized APIs. This is driving significant development work as banks and fintech companies build compliant API layers and third parties build on top of them.

Enhanced Biometric Security

Behavioral biometrics, how you type, swipe, and interact with a device, are being used alongside traditional authentication methods. Financial software in 2026 increasingly incorporates continuous authentication rather than single point-of-login security.

Common Mistakes That Sink Financial Software Projects

There are patterns that come up again and again when financial software projects fail or go significantly over budget. Here are the most important ones to avoid.

● Starting development before compliance requirements are mapped. This is consistently the most expensive mistake teams make. Database schemas designed without audit trail requirements, authentication flows built without role-based access controls, and API endpoints created without proper logging all need to be rebuilt later. That rework costs far more than getting it right during the design phase.

● Underestimating compliance timelines by 50% or more. Security and compliance work almost always takes longer than initially planned. Budget for it appropriately from the start.

● Skipping the discovery phase to save money. Thorough discovery almost always reduces total project cost by preventing expensive scope changes mid-development.

● Choosing a development partner based purely on hourly rate. Financial software requires specialized domain expertise. A lower hourly rate from a team without financial industry experience will cost more in the long run through rework, compliance gaps, and integration failures.

● Treating security as a final step. Security architecture needs to be established in the first sprint, not the last.

● Not planning for data migration costs. If you are replacing a legacy system, data migration alone can consume 20-30% of your total project budget.

Answers to Common Questions About Financial Software Development

What is the difference between fintech software and financial software?

Fintech software typically refers to technology-first financial products, think apps like Stripe, PayPal, or Robinhood, that use software as the core business model. Financial software is a broader term that includes any digital system used to manage financial processes, from enterprise accounting platforms to banking cores. In practice, the line between them has blurred significantly in 2026. Modern financial software uses the same technologies and architectural approaches as leading fintech products.

How long does it take to build financial software?

Timeline depends heavily on complexity. A basic MVP with core features typically takes 3-4 months. Mid-complexity platforms with multiple integrations, compliance workflows, and analytics usually take 5-8 months. Enterprise-level financial systems with fraud detection, multi-region compliance, and complex integrations require 8-12 months or more. Each third-party integration (payment gateways, banking APIs) typically adds 2-4 weeks to the timeline.

What compliance does financial software need in 2026?

It depends on what your software does and where it operates. PCI-DSS is required for anything that processes or stores card data. GDPR applies to any business handling personal data of EU residents. SOC 2 is important for any SaaS financial product. AML and KYC requirements apply to platforms that onboard financial customers or process transactions. Always map your compliance requirements before writing a single line of code.

Should I build custom financial software or use an existing platform?

If your processes are standard and well-covered by existing tools, buying off-the-shelf and customizing through configuration is faster and cheaper initially. If your business logic is proprietary, your integrations are specialized, or your compliance requirements demand full data control, custom development is the right path. Many businesses in 2026 use a hybrid approach: off-the-shelf for standard functions, custom for competitive differentiation.

What technologies are used in financial software development?

Common choices in 2026 include React or Angular for frontend web development, React Native or Flutter for mobile, Python or Java for backend processing, PostgreSQL for transactional data storage, Apache Kafka for real-time event processing, and AWS, Google Cloud, or Azure for cloud infrastructure. AI components typically use TensorFlow or PyTorch. The exact stack should be chosen based on your specific requirements, not just current trends.

How do I choose a financial software development company?

Look for demonstrated experience in financial software specifically, not just general software development. Ask about their compliance experience with the frameworks relevant to your project. Evaluate their security practices and whether they conduct independent security audits. Check references from financial services clients. Assess their discovery and architecture planning process. A team that rushes to coding without thorough discovery is a red flag in financial software projects.

Digisoft Solution: Top Financial Software Development Partner

At Digisoft Solution, we have spent years building secure, scalable, and compliance-ready software for businesses in the financial services space. We understand that financial software is not like building a marketing website or an e-commerce platform. The stakes are higher, the complexity is real, and the margin for error is essentially zero.

Here is what working with Digisoft Solution looks like in practice.

We Start With Compliance, Not Code

Before any architecture is designed, we map your regulatory requirements. Which compliance frameworks apply to your project? What does your data residency situation look like? What audit trail requirements need to be built into the database schema from day one? These are the questions we answer in our discovery phase, because getting them right upfront is what prevents expensive rework later.

Security Architecture That Is Built In, Not Bolted On

Our security-first approach means encryption, access controls, tokenization, and anomaly detection are part of the initial architecture, not features added after the core build. We conduct independent security audits and penetration testing as part of every financial software project, not as optional add-ons.

Full-Stack Financial Software Development

Our team covers the entire stack, from UI/UX design for financial interfaces to backend systems that handle high-volume transaction processing, from payment gateway integrations to AI-powered fraud detection modules, from cloud infrastructure setup to ongoing maintenance and support.

Integration Expertise Where It Matters Most

We have experience integrating with major payment gateways, banking APIs, KYC/AML providers, credit bureaus, and enterprise systems. We know where integration projects tend to get complicated and how to plan for that complexity from the start rather than discovering it mid-project.

Our Financial Software Development Services Include

- Custom Fintech Application Development

- Digital Banking Platform Development

- Payment Gateway and Processing System Development

- Lending and Credit Platform Development

- Accounting and Financial Management Software

- AI-Powered Fraud Detection Systems

- RegTech and Compliance Automation

- Financial Software Security Audits

- Legacy System Modernization

- API Integration for Open Banking

If you are planning a financial software project and want to talk through the requirements, our team is ready to help. We offer a free initial consultation to assess your project scope, identify compliance requirements, and give you a realistic picture of what the build actually involves.

Frequently Asked Questions

Is financial software development regulated?

Financial software itself is not regulated in the same way a bank is, but the systems that touch financial data must comply with a range of regulations depending on their function and the jurisdictions they operate in. PCI-DSS applies to payment processing. GDPR applies to personal data handling in Europe. AML and KYC regulations apply to customer-facing financial platforms. Your development company should be familiar with the specific compliance requirements for your project type.

Can I use AI in my financial software?

Yes, and in 2026 you really should be thinking about it seriously. AI is being applied in financial software for fraud detection, credit scoring, customer support through chatbots, predictive financial analytics, document processing, and compliance monitoring. The key is implementing AI responsibly with proper data governance, model transparency where regulations require it, and regular model validation to prevent bias.

What is the difference between a payment gateway and a payment processor?

A payment gateway is the technology that captures and transfers payment data between a customer and the merchant's bank. A payment processor is the company that handles the actual transaction between the card network, the issuing bank, and the acquiring bank. In most financial software projects, you integrate with a payment gateway like Stripe, Braintree, or Razorpay that handles the processor relationship for you.

How do I protect my financial software from data breaches?

The protection starts at the architecture level, not in the security settings panel. This means field-level encryption for sensitive data, tokenization of payment details, principle of least privilege for data access, independent penetration testing before launch, continuous security monitoring post-launch, and a documented incident response plan. IBM's data found that financial institutions face average breach costs of $6.08 million per incident. The investment in proper security architecture is significantly less than the cost of a breach.

What is open banking and how does it affect software development?

Open banking refers to regulations and technical standards that require financial institutions to share customer financial data with authorized third parties through secure APIs. For software developers, this creates both opportunities (building on top of banking data) and requirements (if you are a financial institution, you may need to build compliant API layers). In 2026, open banking standards are expanding globally and are an important consideration for any financial software project in regulated markets.

How do I estimate the ROI of a custom financial software project?

ROI calculation for financial software should consider: reduction in manual processing costs and staff time savings, reduction in error rates and associated costs, improved compliance posture reducing regulatory risk, customer acquisition and retention improvements, new revenue streams enabled by the platform, and the avoided costs of vendor licensing as you scale. A well-built custom platform typically delivers better financial performance over a 3-5 year horizon compared to off-the-shelf solutions for complex requirements.

Do I need a dedicated maintenance team after launch?

For any financial software handling real transactions or customer data, yes. Ongoing maintenance covers security patches (which are non-optional in this threat environment), regulatory compliance updates as rules change, performance optimization as transaction volume grows, and new feature development. Plan to budget 15-25% of your initial build cost annually for ongoing maintenance and support.

Final Thoughts: Building Financial Software That Actually Works

Financial software development in 2026 is one of the most technically demanding, compliance-sensitive, and consequential areas of software engineering. Get it right and you build a platform that processes transactions reliably, protects customer data, passes regulatory review, and scales with your business. Get it wrong and you are looking at expensive rework, compliance failures, security incidents, and damaged customer trust.

The businesses that succeed with financial software projects are the ones that invest in proper discovery upfront, choose development partners with genuine financial domain expertise, treat compliance as an architectural foundation rather than a final checkbox, and plan for ongoing maintenance as part of the total cost of ownership.

If you are ready to start a financial software project, or if you are evaluating your current systems and wondering whether custom development makes sense for where your business is heading, we would love to talk. Digisoft Solution offers a free initial consultation for financial software projects. We will assess your requirements, identify your compliance obligations, and give you a realistic picture of what building the right solution actually involves.

Digital Transform with Us

Please feel free to share your thoughts and we can discuss it over a cup of coffee.

Kapil Sharma

Kapil Sharma

Digisoft Solution

Digisoft Solution